Credit unions face a tough challenge: keep services simple and personal, while defending against a wave of complex, fast-moving cyber threats.

This article walks through the biggest risks today, why they’re getting worse, and what you can actually do about them.

Let’s get started.

What’s Holding Credit Unions Back

The job has never been harder. Credit unions are trying to modernize, protect their members, and stay compliant… all with fewer resources than the big players.

Here’s what’s standing in the way:

1. Compliance pressure keeps rising

Cyber rules are tightening across the board. Global regulators now expect faster incident reporting, stronger data controls, and proof that the basics are covered — from risk assessments to breach response.

In many regions, credit unions have just hours to report serious incidents. And the expectations only grow from there.

The problem?

Many credit unions don’t have the tools or processes to detect and respond fast.

Monitoring is spotty. Reporting is reactive. And the gap keeps growing.

2. Staffing gaps are growing

Hiring and keeping skilled cybersecurity staff is tough everywhere. For credit unions, it’s worse. They can’t always match salaries from bigger institutions.

Some credit unions don’t even have a dedicated security team. Others rely on one or two overworked IT staff to do it all. Even those with cybersecurity talent often lack the tools or budget to act fast.

Security operations are harder than they were two years ago — and they weren’t easy then.

3. Legacy systems drag everything down

Most credit unions still run on aging infrastructure. That means unpatched systems, manual work, and zero visibility into real-time threats. Many don’t have proper email security. Others can’t segment access or detect lateral movement.

When that infrastructure holds sensitive member data, the cost of falling behind is much more than downtime… It’s exposure.

4. The pressure to modernize never stops

Members expect fast, easy, digital banking. Boards want innovation. Regulators want proof of control. But credit unions are still working with limited teams, old tech, and tight budgets.

This slows down modernization — and it shows.

5. Younger generations are tuning out

The average credit union member is over 47. That number hasn’t changed much in years. Younger consumers want mobile-first, digital-native experiences. Without them, credit unions lose future growth — and relevance.

The Cybersecurity Challenges Credit Unions Can’t Ignore

Cyber threats are changing faster than most credit unions can react.

Attackers are more advanced, more automated, and no longer just going after big banks. They’re targeting the vulnerable — and that includes smaller, under-resourced institutions.

Here are some of the biggest challenges credit unions face:

1. The digital footprint is growing too fast

Every mobile app, online portal, cloud integration, or third-party service adds exposure. Credit unions rely on vendors for speed and scale, but each one brings additional risk. Many don’t have full visibility into where data flows, who has access, or how securely vendors operate.

Attackers love this kind of fragmentation. It gives them more paths in — and fewer eyes watching.

Learn more about External Attack Surface Management here.

2. Outdated systems are wide open

Unfortunately, legacy tools weren’t built for today’s threats. Many credit unions still run core systems without modern protections like real-time visibility, endpoint detection, or behaviour analytics. That means attackers can get in and move around without being seen.

These systems don’t just slow things down; they leave the door open.

3. Incident detection is too slow

You can’t stop what you can’t see. And most credit unions don’t have 24/7 monitoring, automated threat detection, or clear escalation paths when something goes wrong.

Without fast alerts/detection and a clear response plan, incidents spread, costs rise, and damage multiplies before anyone knows what’s happening.

4. Cyber insurance keeps raising the bar

Getting covered used to be simple. Not anymore. Carriers now want proof of strong controls — not just firewalls, but full visibility, access policies, staff training, and tested response plans.

Premiums are rising.

Requirements are tougher.

And without a mature cybersecurity program, credit unions may struggle to qualify at all.

5. Vendors create supply chain risk

Third-party platforms and service providers are now prime targets. A single breach at a vendor can ripple into dozens of credit unions. And most institutions don’t have the capacity to vet every partner’s security posture or monitor them over time.

Check out this article about Third-Party Risk Management.

6. Reporting is fragmented and reactive

Many credit unions don’t have standard processes to detect, document, or escalate cyber incidents.

The result?

Delayed action, regulatory risk, and major recovery costs. Some can’t even tell when a breach starts — they only find out when it’s too late.

7. Manual defence can’t keep up with AI threats

Threat actors are using AI to launch faster, smarter attacks, including deepfake voice calls, tailored phishing, and automated credential stuffing.

Defending against this with manual tools, old alerts, or once-a-day scans is, of course, slow but also dangerous.

Credit unions need defences that move just as fast.

The Top Cyber Threats Credit Unions Face Now

Threat actors don’t need a million-dollar budget to hit hard. They use stolen logins, fake voices, malware kits, and human error. And they’re aiming straight at the institutions with the least room for failure.

Here are the threats hitting credit unions right now:

1. Phishing and social engineering

Still, the number one entry point for most breaches. Attackers spoof executives, vendors, or even members to trick staff into clicking, sharing, or wiring money. And with AI, phishing emails are more convincing than ever.

No firewall can fix poor judgment — training helps, but it’s not enough on its own.

2. Ransomware

If your systems go down, your members feel it immediately. That’s what makes ransomware so damaging for credit unions. Attackers encrypt your data and demand huge payouts, knowing you can’t afford long outages.

Backups help. So does containment. But without both, you’re stuck.

3. Insider threats

Sometimes the breach starts inside. A careless employee clicks the wrong link. A third-party contractor has too much access. Or worse — someone inside wants to cause harm.

You need visibility into access, activity, and unusual behaviour before it becomes a crisis.

4. Supply chain attacks

Credit unions work with dozens of vendors for payments, lending, IT, and analytics. If just one of them gets hit, your member data and operations are at risk.

Attackers look for the weakest link in the chain. And they don’t care if it’s not yours.

5. Voice cloning and deepfakes

AI-generated audio is being used to impersonate executives or support agents. One fake call is enough to trigger a password reset or money transfer — if your staff isn’t ready.

This isn’t theoretical anymore. It’s happening.

6. Credential theft and account takeovers

Stolen logins fuel everything from wire fraud to internal access. Attackers target executive credentials, member portals, and admin accounts — anything that can get them in quickly and quietly. Btw, here is how you can keep your sensitive information safe.

Credential stuffing, MFA fatigue, and reused passwords all make it worse.

7. Dark web exposure

Member info, staff logins, fake websites, phishing kits — they’re all for sale on the dark web. If your breach hasn’t happened yet, it might already be in motion.

Dark web monitoring can give you an early warning, but only if you’re watching.

We wrote an article to learn everything about dark web monitoring, check it out here.

8. Credit card fraud

Stolen card numbers, fake purchases, chargebacks — credit unions deal with this daily. It’s not always a data breach — sometimes it’s a downstream effect of a bigger breach elsewhere. But the impact still lands on your team.

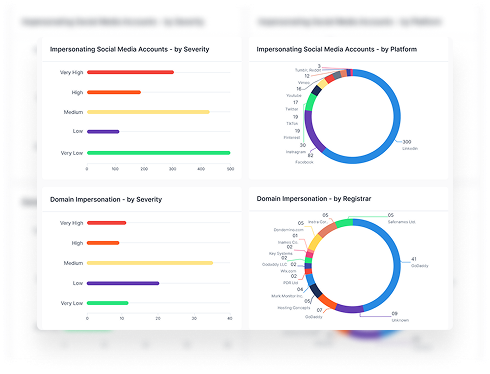

9. Brand impersonation

Fake social media accounts, spoofed websites, bogus support numbers. Attackers mimic your brand to trick members into giving up info or money, and it damages trust fast.

Brand monitoring and takedown services help, but most credit unions don’t have them in place.

10. Malware and remote access trojans

These old-school attacks still work. A single click on the wrong link can install a keylogger, open a backdoor, or give an attacker full control of a staff machine. Many small orgs don’t even know it’s happening until weeks later.

What Happens When a Credit Union Gets Breached

Most credit unions think it won’t happen to them — until it does. Then everything shifts.

One breach doesn’t just expose data. It shakes member trust, disrupts operations, and pulls leadership into weeks of damage control.

Here’s what follows when things go wrong:

1. Member disruption happens fast

When systems go down, so does trust. Members lose access to their accounts, cards stop working, support lines get slammed — and suddenly, your credit union looks unreliable.

Even if no data was lost, the damage is done.

2. The financial fallout adds up

Breaches are expensive. Legal help. PR crisis teams. Third-party forensics. System restoration. Insurance deductibles. Fraud refunds. It adds up fast, often into six or seven figures.

And that’s before you get hit with regulatory fines or civil suits.

3. Regulators come knocking

Regulators want answers, fast:

What happened?

When did you find out?

What have you done since?

In many cases, credit unions have as little as 72 hours to report. Miss the deadline, and you risk fines, audits, and reputational fallout.

4. Members don’t wait around

Trust is everything. And once it’s shaken, it’s hard to get back. Especially with younger members, who expect always-on, app-level service. One bad experience, and they’re gone.

5. Competitors move in

In the wake of a breach, nearby banks and fintechs often ramp up offers and promotions to pull your members away. Timing isn’t a coincidence.

Why Credit Unions Need Modern, AI-Driven Cybersecurity

Credit unions run on trust. That trust used to live across the counter — now it lives online.

Members expect digital services to be safe, fast, and smooth. Regulators expect airtight controls. Threat actors expect you’re behind. And they’re right — most legacy tools just can’t keep up.

That’s where modern, AI-driven security comes in.

1. Legacy tools miss too much

Old platforms flood teams with noise, false positives, and alerts that show up after the damage is done. They weren’t built for cloud, mobile, or AI-powered threats.

2. AI keeps up with the pace of risk

AI systems scan everything, including social, cloud, news, web, and dark web, and flag risks in real time.

No delay.

No manual triage.

Clear signals that help your team act quickly.

3. Sensitive data demands stronger controls

Credit unions handle member info, financial records, and identity data.

One mistake can break trust, but it also brings legal and regulatory pain.

4. Small teams need smarter support

Most credit unions don’t have a 24/7 security team. AI closes that gap — surfacing the real threats, automating takedowns, prioritizing risks based on business impact, and cutting the noise.

5. You need fast, easy onboarding

You shouldn’t wait months to get protected. The right platform gets you live fast, without ripping out your stack or draining your time.

6. You need prioritization

AI tools rank threats by potential impact, so you know where to act. Limited resources go further when you focus on what matters most.

7. Sentiment matters, too

Modern security includes social listening. If members are losing trust or attackers are spreading disinformation, you’ll see it early and respond fast.

Learn more: The Future of Digital Risk Protection

What To Look For In a Cybersecurity Platform (That Actually Works For Credit Unions)

Most cybersecurity platforms weren’t built for credit unions. They assume you’ve got a big security team, unlimited budget, and months to roll out. You don’t.

You need tools that move fast, cut the noise, and give you real-time visibility, without wasting time or making your life harder.

Here’s what matters:

1. AI-powered threat detection

Credit unions should look for a platform that uses AI to surface phishing attempts, impersonation, deepfakes, and leaked data in real time. It should scan your entire digital surface, including your website, social media, employee accounts, and more.

Because if you can’t see it, you can’t stop it.

2. Smart prioritization with risk scoring

Most tools overwhelm small teams with endless alerts. You need something smarter — a platform that scores risk based on business impact, not just volume. It should tell you what’s urgent, what can wait, and why it matters.

This is how small teams stay focused without falling behind.

Learn everything about the Risk Scorecard here.

3. Executive protection

Key members and leaders are prime targets for impersonation, social engineering, and data leaks. The platform you choose should flag threats tied to specific individuals and provide tools to prevent them from escalating.

Because when an executive gets hit, it’s not just personal — it’s brand and business risk too.

4. Dark web monitoring

You won’t find every threat on the surface web. A complete platform monitors the deep and dark web for stolen data, leaked credentials, impersonation kits, and attack planning. It should give you early warning before those risks impact your business and reputation.

5. Takedown automation

Fake domains, cloned social profiles, leaked documents — you need them gone fast. A good platform should let you submit takedown requests with one click and track the resolution.

Manual takedowns waste time. Automation lets you stay ahead.

6. Real-time reporting and compliance tools

Regulations are moving fast — and they’re not slowing down. You need clean logs, audit trails, and evidence to prove your team acted quickly and responsibly.

Look for a platform that makes reporting simple — with export-ready data you can share with your board, regulators, or insurer without last-minute chaos.

7. 24/7 visibility across assets

Websites, cloud platforms, employee devices, third-party vendors — your digital environment is bigger than it looks. You need continuous monitoring across all of it, so nothing falls through the cracks.

Credit unions don’t have extra cycles to chase blind spots.

8. Support built for small teams

Skip the bloated dashboards and complex workflows. Look for a platform that gets to the point — with built-in guidance, clear actions, and support that speaks human. Credit unions need speed and clarity, not busywork.

Best Practices And Priorities Moving Forward

You don’t need five tools doing half the job. You need one approach that covers the gaps, supports your team, and keeps you a step ahead.

Here’s how to move forward with focus:

1. Have a real plan — not just a policy

When something breaks, people look for leadership. Have a clear, tested incident response plan — not a dusty PDF.

Everyone should know what to do, who to call, and what happens next.

2. Know where you stand

You can’t improve what you haven’t measured. Get a real picture of your external exposure — what’s visible, what’s vulnerable, and what to fix first.

Get started with a free Digital Risk Scorecard.

3. Train your people

Human error is still the top attack vector. Regular training on phishing, social engineering, and MFA hygiene goes a long way. Make security part of everyone’s job — not just IT.

4. Monitor exposure continuously

Don’t wait for an alert to tell you something’s wrong. Monitor your digital footprint, vendor risks, and dark web mentions in real time.

The earlier you spot a threat, the easier it is to contain.

5. Review vendors and third-party risk

Your vendors are part of your attack surface. Make sure you know what they’re doing to protect your data — and what gaps they might expose you to.

6. Update what’s outdated

Legacy systems create risk. If something’s unsupported or unpatched, it’s a liability, not just a slow process. Prioritize upgrades where they matter most.

7. Invest in real-time detection

Static reports and once-a-week scans won’t cut it. You need live detection that actually sees what’s happening, not just what already happened.

8. Cut down the noise

You don’t have time to chase every alert. Use tools that reduce false positives, flag what matters, and help you act fast, not just stare at dashboards.

9. Align security with business outcomes

Security isn’t just about compliance. It’s about uptime, trust, and growth.

Make sure your efforts support the big picture, not just the checklist.

10. Build a security-first culture

Policies help. Training helps. But mindset matters most. Security should be part of every decision, from vendor onboarding to launching a new feature.

Got questions?